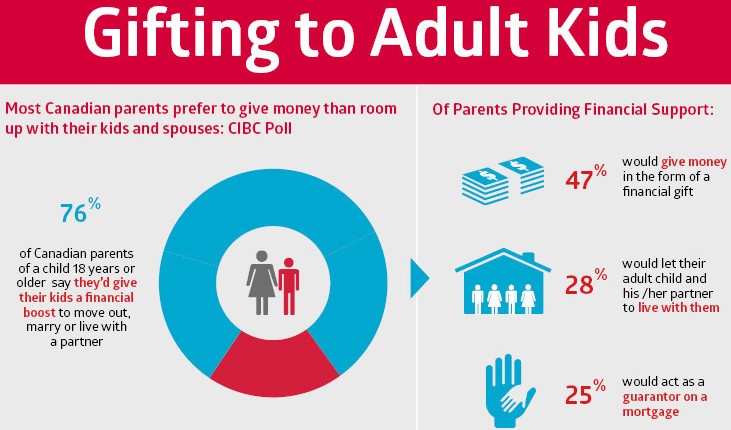

I often get the question, “is it better for me to give money now, while I’m alive?”. A very understandable query particularly from our clients. Many we project, will have more assets than they will need in their lifetimes. The deeper seeded reason for someone asking such a question though is that many of us in our later 50’s through 70’s may be seeing our kids struggling to meet all of their expenses; or we simply want to make life a lot easier for them.

What joy a parent (or grandparent) can give by handing down money to an adult child, right? The reality though is that in many cases we just want to ease our own pain. Having the ability to relieve that uneasiness can be so easy. Just throw some money at the problem and it all goes away. That may be, however it may not actually be a good thing to do.

This is something that has struck me personally within my own family. An introspective look helped me realize I was giving to help but it was just as much to ease my own discomfort in seeing them in a situation. Sometimes I succumbed to this urge and other times I didn’t. More often than not, refraining was the best thing to do, when you look back holistically. A cactus will flower after a dry and stressful period. They’ll die with too much watering.

With being said, below you’ll find some ins and outs of passing money on….

First consideration is the “Attribution Rules” – There is tax to pay no matter who owns the asset. Who will the tax liability then fall to? Before you do anything you have to know the tax implications will be. Most of us will be giving money or an asset that is held personally however, money can be given from within a corporation as well.

No matter where the money is currently sitting, if it is gifted to a related minor (e.g., child grandchild, niece or nephew), any future “income” (interest, dividends or rental income) made on the investment will be taxed in the giver’s hands (parent or grandparent) until the minor reaches the age of 18. If there are any gains made while the minor holds it, that tax liability falls on them (currently only 50% of capital gains are taxable). This attribution of tax liability only lasts while the giver is still alive.

Give Now Or Later? – One of the common beliefs is that it’s best to give money before someone dies because there a “gifting tax” in Canada. That is absolutely incorrect. There is no such tax in Canada other than probate fees which vary by province. So, with that out of the way….

There is a key thing to consider and it comes from the lesson we get every time we board a plane and are waiting for take off. Our own survival gear should be in place before we try helping someone next to us. I’ve read about and seen many examples of people giving money to their kids at the expense of their own financial stability. Frankly, that’s foolish. In our own family, when my parents sold their house and downsized considerably, I was asked by one of my siblings why I thought mom and dad weren’t handing down some. They seemed to have more than they needed. I pointed out that they may need it for later and, if they fell short, I didn’t want to negotiate between us as siblings, how we were going to make up the shortfall. So before any money is handed down to the next generation, make sure projections have been done by your Financial Planner that you will have enough for your own needs both seen and unseen. This will ensure you have your living and lifestyle expenses met before you siphon money off to your kids and grandkids.

Putting Adult Children On Title of Your Principal Residence (Joint Ownership) – Simply put, it’s a bad idea. The reason most people will want to do it though is to save on probate fees. Since a home is often the largest personal asset, what could make doing this a bad idea? Probate fees in BC are 1.4% for any part of an estate over $50K (Nova Scotia, BC & Ontario have the highest probate fees). Yes, that can add up to a lot of dollars. The biggest financial caveat is that it puts the tax free capital gains on a principal residence at risk. Eg. if 1 adult child is added to the ownership when the home is worth $1 million and then, when the parent dies, it is worth $1.5 million, $250K of capital gains faces income tax to the adult child (this assumes they had their own home already or purchased one while their parent was still alive). You can get around this issue by setting up a “bare trust”. This however can be more cost and hassle than it is worth. As well, there are a handful of potential logistical drawbacks (which can be quite damaging). I’ll leave it at that. Let’s move on to a few other areas of passing money down…

Give Them Investments? – Sure, go for it. If you do that though on an investment that is worth way more than you paid for it, you’re going to trigger a capital gain. Why? Because in CRA’s eyes, giving this money is viewed as you having sold the investment (a “deemed disposition” is what CRA calls it). Sure you could be lightening your tax bill going forward but you will get a tax hit in the year you gift it.

Giving To Children But Not Letting Them Control The Money – This is where an “Inter-vivos” Trust comes in. One specific reason to use this kind of legal entity is for those you think aren’t good with money; “they’ll just burn through it”. It can also be set up for someone who has a disability. Also, it can be used to protect the assets from going into a less than stable marriage relationship and having 1/2 ending up in your offspring’s spouse’s hands.

The money that you give goes into an Inter-vivos Trust. You appoint Trustees for the Trust who will decide on how the money is funneled to your beneficiaries. This will be based on the parameters that you stipulated. The Inter-vivos Trust is in place and operating while you are alive. You can also have a Testamentary Trust set up upon your death, through your Will. It can continue the management and the passing down of your assets after you are gone.

Passing Money On To A Charity – This is an adjunct to the titled topic and I wanted to include it for 2 primary reasons: 1) it has to do with passing money down and 2) many of us have way more than our offspring could ever really need so why not enrich society and other people’s lives by directing it to other causes, in a tax efficient manner?

Giving money to a charity can be done regularly and I highly recommend getting into the habit of doing this. I’m talkin here about giving money intentionally and materially rather than sporadically and without any real thought (eg. at the checkout of a grocery store). It can be done out of your own cash flow (which only costs you ~52% of what you are giving, after factoring in your tax savings). You can also give a part of an investment you hold and save even more. Cheryl and I have been doing the latter lately on virtually all of our charitable donations. Like giving to your younger family members while you are alive, this gives you the benefit of seeing the money put to good use, producing a higher level of gratification and joy. Your willingness to give will open your eyes to the right opportunity and you’ll find it giving back to you immensely as well. This has been the case for me, personally.

These are just some of the variations to fit your specific circumstances and desires. If you have questions (or you don’t have a Financial Advisor who talks holistically with you about your finances) we can help develop a plan that fits your needs and wants. Please contact our office.

PS. Here is a great article in the Financial Post on this entire topic.